Why the FDIC exists

Most people have one of three perspectives on the FDIC

Most people have one of three perspectives on the FDIC- U.N. sponsored gummint agency, that makes black helicopters for use by the Trilateral Commission

- Something to do with medicine approval?

- Something to do with regulating banks?

As it turns out, there is actually a perfectly valid reason for the existence of the FDIC - and it has to do with Banks, and Nash Equilibrium.

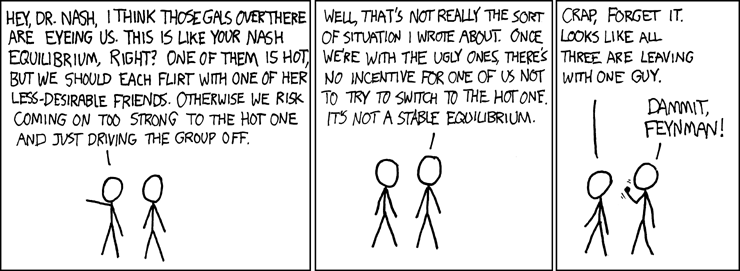

To put it simply, a Nash Equilibrium is the equivalent of a self-reinforcing law, i.e., one that nobody has an incentive to break, despite the absence of a police force, because you end up worse off breaking it than if you don't.

Or ask XKCD puts it

"What on earth does the above have to do with the banks?"

I'm glad you asked.

Being a bank, what it does is takes in short-term deposits from people (you, I, Alice down the street, etc.), and lends it out as long-term loans to local businesses.

The above is key, and is worth elaborating on. Short-term deposits are things like your paycheck. It gets deposited on the 1st of the month, and you take it out in small chunks during the month to pay rent, get groceries, etc. Long-term loans are things like construction loans to local businesses, which might get paid back only over a ten year span, as compared to my short-term deposit.

As a first-order approximation, Zelda's Bank keeps 10% of all the short-term deposits as cash, and lends out the remaining 90%. This 10% suffices to cover any sudden up-tick in people needing money (emergency surgery, trip to see your parents in India, that darling Prada purse you simply must have, etc.). But, by definition, 10% of the short-term deposits are only 10% of the short-term deposits, and not 100% - this is important, as you'll see in just a moment.

One Monday morning, John is getting his morning-coffee at Starbucks, when he thinks he overhears someone say that Zelda Bank's construction loans were not properly vetted, and are going bad. Being a fiscally prudent guy, he promptly heads over to Zelda Bank to get his money out, but also being a nice guy, he calls up a couple of his friends, and tells them to do the same. His friends call their friends, and the next thing you know, the entire town is headed over to the bank to get their money out.

Enter the FDIC. At the core of it, the FDIC sez. "We, the Gummint, will guarantee that the first $250,000 of your money in the bank will get paid back, even if the bank goes kaput".

And that simple act changes the dynamics completely.

John hears the rumor, blah blah blah, but instead of blasting over to the bank, John sez. "meh, there will probably be a bunch of people over at the bank clamouring for their money, I'll just take a nap instead, and head over next week when the chaos has died down". His friends will all probably do exactly the same thing, resulting in virtually nobody blasting over to the bank. In short, the Nash Equilibrium here is for there to not be a Bank Run!

This remarkably obvious (in retrospect!) take on Bank Runs was actually formalized in 1983 by Douglas Diamond Phillip Dybvig in a seminal paper and is now immortalized as the Diamond-Dybvig model.

And that my friends, is why the FDIC exists, and why Bank Runs don't really happen anymore. Or if they do, why they tend to be really, really short-lived! Exhibit A is the Northern Rock bank run which continued till the British Government guaranteed the deposits FDIC style, at which point the Run vanished...

Comments